The price on the contract is never the figure that lands in your account. Between the cost of selling, the duty on what you buy next, and the gap before everything settles, a downsizing move sheds more than most owners expect — and the number that matters is the one you keep.

In thirty-five years of handling sales across the Eastern Suburbs, I have watched the same quiet moment play out at more kitchen tables than I could count. An owner has decided to downsize. They know roughly what their home is worth, they know roughly what the apartment they want will cost, and they have done the subtraction in their head. The gap, they assume, is what they will have to live on.

It is almost never that simple. The contract price is a gross figure. What you actually walk away with — the money free to fund the rest of your life — sits well below it, and the distance between the two is where most of the anxiety, and most of the avoidable mistakes, live.

So let me walk through it the way I would at your table: in the order the costs actually arrive.

What it costs to sell my home

The largest line is agent commission. In the Eastern Suburbs it commonly sits around two per cent of the sale price, though it is negotiable in every case and tends to soften on higher-value homes. The figure people forget is the GST on top — ten per cent of the commission itself. On a sale of four and a half million dollars, a fee of one-point-eight per cent is eighty-one thousand dollars, and the GST lifts it past eighty-nine thousand.

Then the campaign. A competitive Eastern Suburbs marketing spend runs somewhere between four and eight thousand dollars; styling the home for sale, which genuinely moves the result in presentation-sensitive streets, adds another two-and-a-half to six thousand. Conveyancing on the sale is modest by comparison — a couple of thousand dollars including the searches. If you still carry a mortgage, the lender charges a few hundred to discharge it; most of the downsizers I work with own outright, so I will set that aside.

Call the cost of selling, on that four-and-a-half-million-dollar home, somewhere near one hundred and five thousand dollars. The contract says four-point-five million. Your net sale proceeds are closer to four-point-three-nine.

What it costs to buy an apartment

Here is the figure that surprises people most, and it falls on the purchase, not the sale. Transfer duty — stamp duty — is the single largest transaction cost in the entire move, and you pay it on the apartment you are buying.

The rates are set by Revenue NSW and they climb steeply. On a purchase of two-point-six million dollars, the duty is roughly one hundred and twenty-five thousand dollars — close to five per cent of the price, paid to the state before you have hung a single picture. Buy higher and it bites harder: above the premium threshold of three-point-seven-two-one million, every additional dollar is taxed at seven per cent. I tell clients to run their exact figure through the Revenue NSW calculator before they fall for anything, because the duty can quietly redraw the budget.

Add the buyer’s conveyancing and the strata and building reports — another two-and-a-half thousand or so — and the cost of buying that apartment lands near one hundred and twenty-seven thousand dollars.

The gap in the middle

There is one more cost that appears on no invoice: the gap between selling and buying. Buy before you sell and you may carry two properties briefly, or lean on bridging finance — which lenders extend cautiously to retirees without an earned income. Sell before you buy and you risk a stretch with the money in the bank and nowhere settled to live. Which way round you do it is a strategy in itself, and one I will take up separately. For now, simply know that the sequence carries a price, and it belongs in your sums.

The arithmetic that matters

Put it together. A home sold for four and a half million. An apartment bought for two-point-six. On paper, a gap of one-point-nine million. In practice:

An illustrative Eastern Suburbs move

Sale price of the family home $4,500,000 (Bellevue Hill, Dover Heights, Rose Bay $7 to $10 million average)

Less the cost of selling−$105,000

Less the new apartment−$2,600,000 (Bondi Junction area) ($6.5 million to $7.5 million 3 bedroom unit in Bellevue Hill, Rose Bay)

Less the cost of buying−$127,500

Free to redeploy≈ $1,667,500

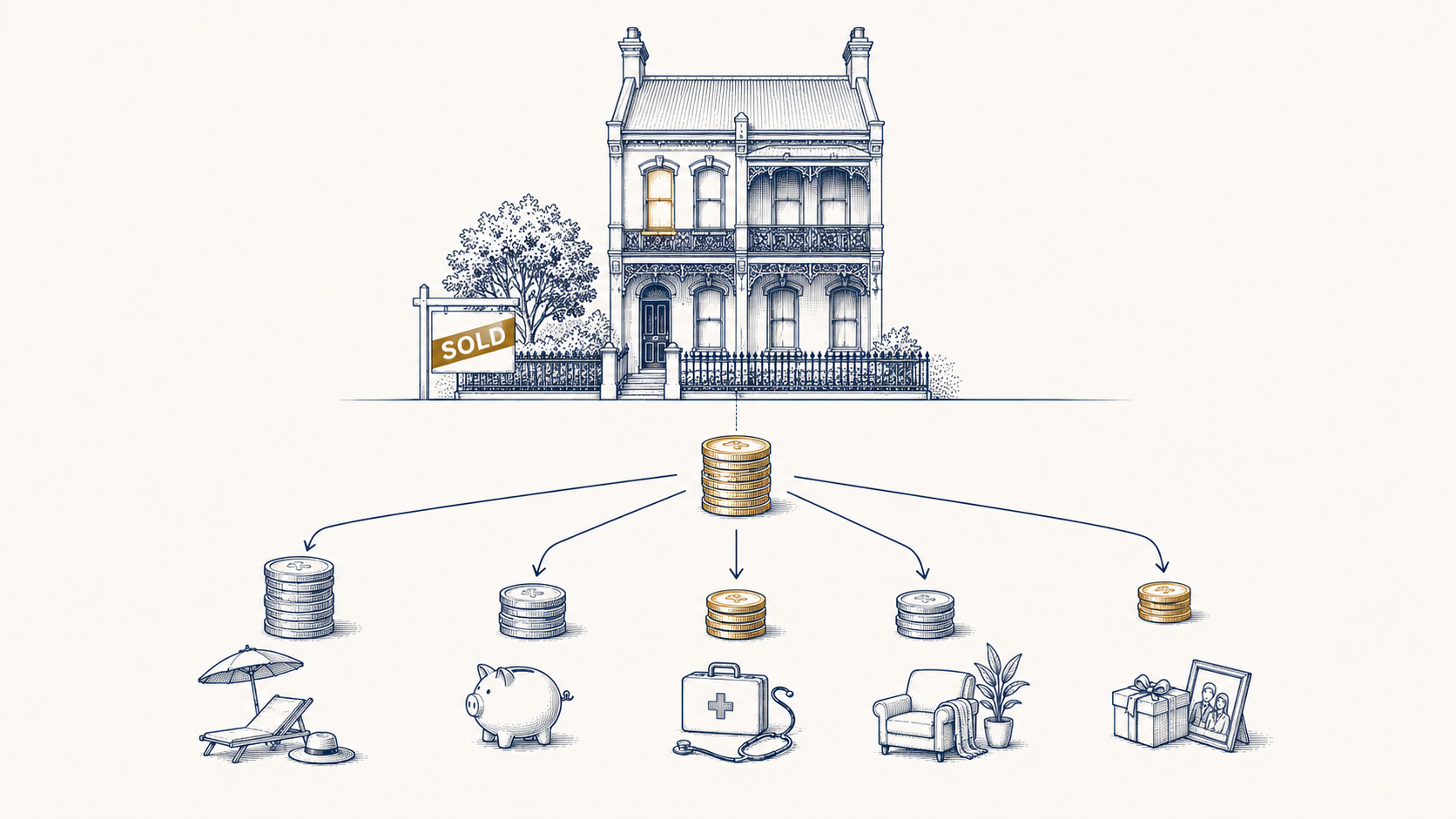

The contract suggested one-point-nine million of headroom. What is actually free to fund your retirement is closer to one-point-six-seven. The quarter of a million in between went nowhere improper — to commission, to GST, to the state, to the professionals who make a clean settlement possible. But had you planned around the headline gap, you would have found yourself a quarter of a million dollars short of your own expectations.

One relief, and one decision

The relief first. The home you are selling is almost certainly your main residence, and a main residence is generally exempt from capital gains tax. For most downsizers the sale itself triggers no CGT — worth stating plainly, because people often brace for a tax that never comes.

The decision is what to do with what remains. If you are fifty-five or older and have owned the home for at least ten years, the downsizer contribution lets you place up to three hundred thousand dollars per person — six hundred thousand for a couple — into superannuation from the proceeds. It sits outside the usual contribution caps, it can be done once, and the money must go in within ninety days of settlement. You need not even buy a cheaper home to qualify. For the right household it is among the most useful moves available, but it rewards planning before settlement, not after.

A word on the Age Pension, since it is always raised. Your family home is exempt from the assets test; the cash you free up is not. For owners selling at the values common in our part of Sydney, the pension is usually beyond reach regardless — the live questions are superannuation and tax, not Centrelink. For those downsizing from more modest homes it matters a great deal, and any change must be reported to Services Australia within fourteen days.

Why I start here

I open with the money because it is the part most often guessed at, and the part where a wrong guess does the most damage. A downsizing move is rarely about trading space for cash. It is about freeing the right amount of capital, at the right time, without an unwelcome surprise at settlement — and that begins with knowing the real number, not the one on the board.

Before you list, before you bid, it is worth sitting down and working the figures through properly: your home, your likely purchase, the duty, the costs, the super, what is genuinely left. It is the conversation I would rather have at the start than at the end.