I was sitting down recently with a colleague who had just returned from Melbourne. We began discussing the apartment market — not from a headline perspective, but from a position of underlying structure.

Because that is where the real story sits.

Australia is now in the most aggressive apartment construction cycle in its history. In New South Wales alone, the government has committed to delivering approximately 377,000 new homes by 2029, the majority of which will be medium and high-density apartments.

At the same time, a number of less visible trends are emerging:

- More than 50% of apartment buildings completed between 2016 and 2022 have reported serious defects

- The price gap between houses and apartments has widened to 86%, the largest on record

- Lending conditions have tightened materially, particularly for higher-density stock

- And a growing proportion of buyers are entering the apartment market out of necessity rather than choice

There are also increasingly frequent examples of financial stress within strata schemes — including instances where buyers have received substantial special levy notices shortly after settlement.

None of this suggests that apartments are inherently flawed.

However, it does point to a simple conclusion:

Apartments are not well understood — particularly in the context of long-term financial performance and risk.

This article is intended to provide clarity across that landscape. Not from a theoretical perspective, but from a practical one — based on how these assets behave over time, how they are assessed by lenders, and how they perform under pressure.

Because in the current market, understanding structure is no longer optional.

Apartment Values

When assessing any property, the starting point should always be performance over time.

In the case of Sydney, the data presents a consistent pattern.

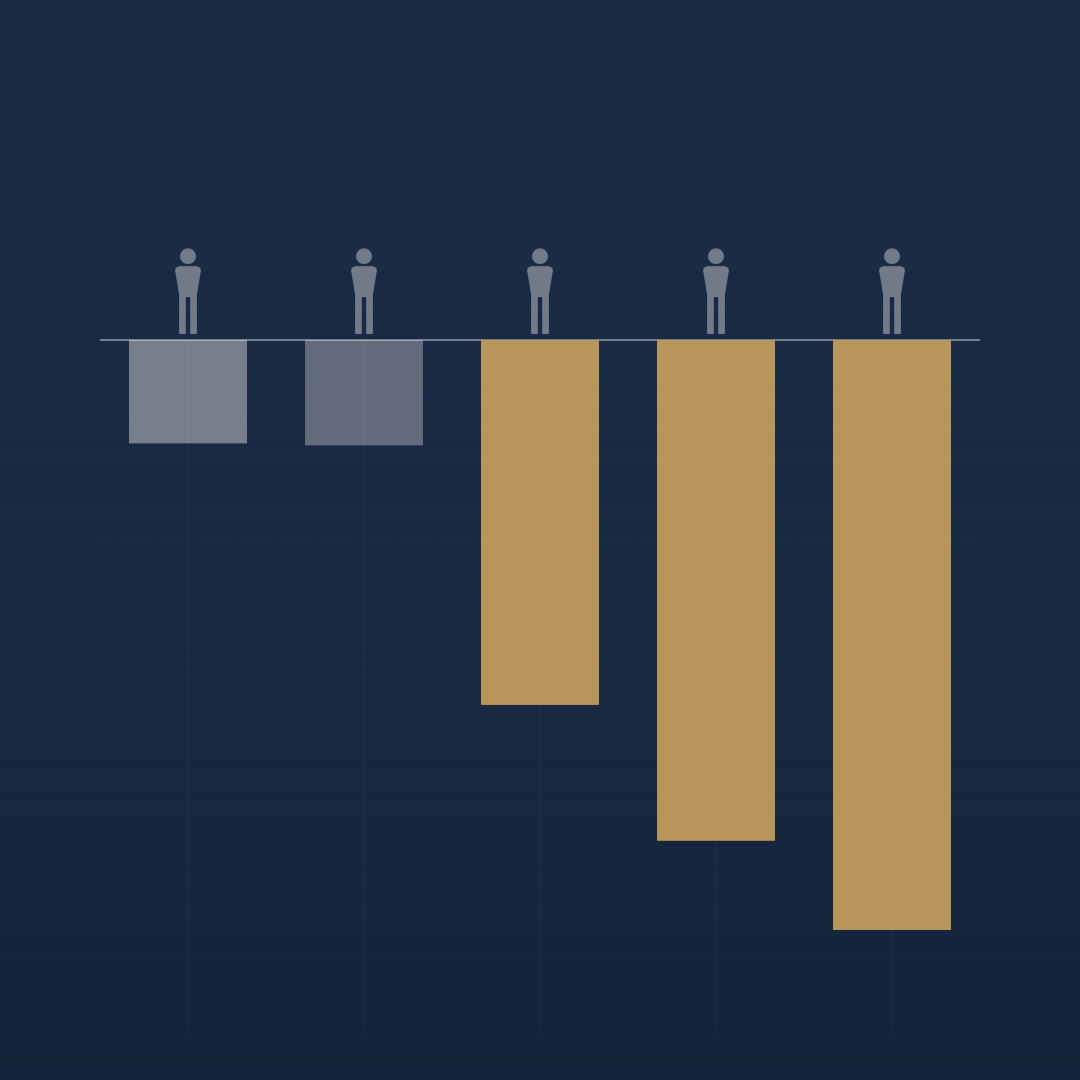

Between 2017 and 2025, median house prices increased by approximately 47%, while apartment values rose closer to 10% over the same period. During the COVID cycle, this divergence became more pronounced — houses gained approximately $239,000 in value, compared to around $65,000 for apartments.

The result is not marginal.

It is material.

Today, the median house price in Sydney sits at approximately $1.6 million, compared to $870,000 for units — a gap of roughly 86%, the widest recorded to date.

This is not a short-term anomaly. It reflects structural differences between the two asset classes.

A house represents ownership of a defined parcel of land — a scarce and finite resource in established suburbs. An apartment represents a fractional interest in a shared building, where the underlying land component is divided across a large number of owners.

At the same time, apartments can be delivered at scale. New developments introduce direct competition to existing stock, often within the same suburb, sometimes within the same street. By contrast, the supply of freestanding homes in established locations is inherently constrained.

Demand dynamics also differ. Owner-occupiers — particularly families — tend to place a premium on land, space, and long-term security. This creates a level of competition in the housing market that is rarely replicated in higher-density apartment stock.

There are also ongoing cost considerations. Strata levies, capital works contributions, insurance, and periodic special levies represent a recurring financial obligation that must be factored into any long-term return.

None of these factors suggest that apartments cannot perform.

However, they do explain why, over extended periods, houses have consistently delivered stronger capital growth outcomes.

Short-Term Dynamics

It is equally important to recognise that the current environment is not entirely one-directional.

Apartments are experiencing a degree of short-term support, driven primarily by affordability constraints.

With house prices sitting beyond the reach of many buyers, demand is naturally shifting toward more accessible price points. This has led to:

- Forecasts of moderate unit price growth between 2025 and 2027

- Rental yields for apartments averaging approximately 4.5%–4.6%, compared to materially lower yields for houses

- Vacancy rates in Sydney remaining tight, supporting rental demand

- Government incentives, including low-deposit schemes, being directed primarily toward the apartment price bracket

These factors are relevant, particularly for investors focused on income.

However, they do not alter the underlying structural drivers.

They are, in effect, responses to affordability pressure — not a redefinition of long-term performance characteristics.

A More Selective Market

The implication of this is straightforward.

Apartments should not be approached as a uniform asset class.

Performance is increasingly dependent on:

- Building quality

- Ownership composition

- Location-specific supply constraints

- Governance and financial management within the strata scheme

Well-located, low-density buildings with strong owner-occupier presence and disciplined financial management can perform very well over time.

Conversely, high-density developments in oversupplied corridors, particularly those built during peak construction cycles, are more exposed to price stagnation, valuation pressure, and ongoing cost escalation.

The distinction between the two is becoming more pronounced.

Closing Perspective on Value

From a real estate agent standpoint, the objective is not to discourage apartment ownership.

It is to ensure that decisions are made with a clear understanding of how these assets behave — not only in favourable conditions, but across the full market cycle.

Because the difference between a sound apartment investment and a problematic one is rarely visible at the point of purchase.

It becomes evident over time.

Oversupply Risks

One of the most common misconceptions in the Sydney market is that we are either “oversupplied” or “undersupplied.”

In reality, both are true — depending on where you look.

At a macro level, Sydney remains structurally undersupplied. The city requires roughly 30,000 new dwellings per year, yet delivery has consistently fallen short of that level. This imbalance is one of the reasons prices have remained resilient over time.

However, that broad statistic masks a more important reality.

At a local level, supply is highly concentrated.

Certain corridors — particularly those aligned with transport infrastructure and large-scale rezoning — are seeing a significant volume of new apartments delivered within relatively short timeframes. In these areas, supply does not arrive gradually. It arrives all at once.

This creates a very different market dynamic.

Instead of competing against a small number of comparable properties, owners may find themselves competing against dozens — sometimes hundreds — of near-identical apartments within the same precinct.

When that occurs, price growth does not necessarily reverse, but it often stalls. Rental competition increases. And when it comes time to sell, liquidity becomes a consideration.

By contrast, established areas with limited development capacity — such as parts of the Eastern Suburbs, Lower North Shore, and Inner West — tend to experience a very different outcome. Supply remains constrained, and demand is driven more by owner-occupiers than investors.

The distinction is critical.

Oversupply in Sydney is not a city-wide issue. It is a location-specific risk.

From a real estate agent perspective, this is where selection becomes essential. Understanding not just the property, but the pipeline around it, is what separates a stable asset from a compromised one.

Defects and Special Levies

If oversupply affects performance, building quality affects certainty.

Over the past decade, this has become one of the defining issues in the apartment market.

The most comprehensive data available indicates that more than half of apartment buildings completed between 2016 and 2022 have reported serious defects. While reforms introduced post-2020 are improving outcomes, a large proportion of existing stock still sits within that earlier cohort.

For buyers, the implication is straightforward.

The risk is not always visible at the point of purchase.

It often emerges later — typically within the first 5 to 10 years of a building’s life, when initial warranties expire and more detailed investigations take place.

When defects are identified, the financial mechanism is the special levy.

These levies can vary significantly depending on the scale of the issue. In some cases, they are manageable. In others, they can be substantial, particularly where waterproofing, façade, or structural works are required.

Alongside this, another pressure point has been building quietly.

Strata insurance costs have increased materially across the market. In some buildings, insurance now represents one of the largest components of annual levies, driven by a combination of construction risk, compliance requirements, and broader market conditions.

Taken together, these factors introduce a layer of financial variability that is not always captured in a standard affordability assessment.

The purchase price is only one part of the equation.

The ongoing cost structure is equally important.

From an advisory standpoint, this is where careful review of the building — its history, its financial position, and its governance — becomes essential.

Lending — What the Bank’s Position Tells You

In many respects, the most objective assessment of an apartment is not the marketing material — it is the bank’s lending position.

Lenders evaluate property through a very specific lens: liquidity under stress. In other words, how easily can the asset be sold if circumstances require it.

Over recent years, that lens has become more conservative, particularly for higher-density apartment stock.

From February 2026, new regulatory settings require banks to limit lending to borrowers with high debt-to-income ratios. At the same time, internal policies across major lenders continue to apply restrictions based on:

- Building density

- Floor area

- Concentration within a development

- Postcode-specific risk profiles

In practical terms, this means:

- Some apartments attract lower maximum loan-to-value ratios

- Others require larger deposits

- And in certain cases, lending may be restricted altogether

For buyers, this is more than a financing detail.

It is a signal.

When a bank reduces its exposure to a particular type of asset, it is reflecting its assessment of that asset’s resale depth and marketability.

This has a direct implication for future liquidity.

If a property is difficult to finance today, it is likely to be difficult to sell tomorrow.

The bank’s view is not just about your loan.

It is an indicator of how the broader market will treat the asset over time.

The Affordability Question

Apartments are often presented as the “affordable” pathway into the market.

On the surface, this is accurate. With a median price materially below that of houses, they provide access to locations that would otherwise be unattainable.

However, affordability needs to be considered in a broader context.

Ownership costs extend beyond the mortgage. Strata levies, insurance, maintenance, and potential capital works contributions all form part of the financial profile.

In many buildings, these costs can range from $13,000 to $30,000 per year, before any major works are required.

For investors, this has a direct impact on net returns. For owner-occupiers, it affects long-term financial flexibility.

At the same time, the buyers most likely to enter the apartment market — first-home buyers and highly leveraged investors — often have the least capacity to absorb unexpected costs.

This creates a structural tension.

The most accessible properties by price are not always the most stable in terms of ongoing financial commitment.

Affordability at purchase does not always translate to affordability over time.

From an advisory perspective, the objective is not to avoid apartments, but to ensure that the full financial profile is understood before a commitment is made.

A Measured Perspective

It is important to maintain balance.

Apartments remain a critical part of Sydney’s housing landscape. In well-selected locations, with strong governance and limited competing supply, they can perform well both as a place to live and as a long-term investment.

The issue is not the asset class itself.

It is the variability within it.

The gap between well-selected and poorly selected apartments is widening, and that gap is driven by factors that are not always immediately visible.

For buyers and investors, the approach needs to evolve accordingly.

Not every apartment will deliver the same outcome.

And in the current market, that distinction matters more than it has in the past.

Government Reform

Over the past few years, New South Wales has introduced some of the most comprehensive building reforms in the country.

These include:

- The Design and Building Practitioners Act

- The Residential Apartment Buildings Act

- The introduction of a dedicated Building Commission

- The iCIRT rating system for builders

- Stronger compliance and inspection regimes before occupation certificates are issued

These reforms are meaningful, and they are improving outcomes — particularly for buildings completed post-2020.

However, there is an important distinction that needs to be made.

Reforms improve future stock.

They do not eliminate the risk embedded in existing buildings.

A large proportion of apartments currently in circulation were built prior to these reforms, and it is within this cohort that most defect-related issues are emerging.

At the same time, there is increasing pressure on the system to deliver new housing at scale. The government’s housing targets require a significant acceleration in construction activity.

This creates a natural tension.

Delivering volume quickly, while maintaining consistent quality, is not a simple equation. It requires discipline across the entire development and construction chain.

From an advisory standpoint, this means buyers need to be very clear about which generation of building they are purchasing into, and what protections — or limitations — apply.

The Role of the Capital Works Fund

If there is one financial metric that deserves close attention in any apartment building, it is the capital works fund.

This fund is designed to cover major future expenditure — lifts, roofing, façades, waterproofing, and structural maintenance. It operates alongside the administrative fund, which covers day-to-day costs.

A well-managed building will typically have:

- A current 10-year capital works plan

- Contributions aligned with that plan

- A balance that reflects future obligations

Where this is not the case, the outcome is usually predictable.

Deferred maintenance accumulates.

Costs increase.

And eventually, those costs are recovered through special levies.

This is where many financial issues begin.

In the current environment, additional pressures are emerging:

- Rising insurance costs

- Higher compliance requirements

- Increased expectations around building maintenance

These are not one-off events. They are structural changes to the cost base of apartment ownership.

The capital works fund is not just an administrative detail.

It is a direct indicator of a building’s financial stability.

When Things Go Wrong

One of the more important changes in recent years has been the introduction of stronger protections for owners facing financial difficulty.

Under updated legislation, owners corporations are now required to:

- Consider payment plans for owners experiencing hardship

- Provide clear information when levies are issued

- Engage in structured processes before enforcement action is taken

These are positive developments.

However, they do not change the underlying obligation.

If a levy is raised, it must be paid.

For buyers, the takeaway is simple.

Risk should be assessed before purchase — not managed after the fact.

Once you are part of a strata scheme, your exposure is shared with every other owner in the building. Your financial position becomes linked to the condition and governance of the entire asset.

Due Diligence

In a market like this, due diligence is not a formality.

It is the difference between a well-positioned asset and a compromised one.

The process does not need to be overly complex, but it does need to be thorough.

At a minimum, every buyer should clearly understand four areas:

1. Financial Position of the Building

- Current capital works fund balance

- Alignment with the 10-year plan

- History of levy increases or special levies

2. Building Quality and Risk Profile

- Age of the building and construction cohort

- Any known or emerging defects

- Compliance with current building standards

3. Lending and Market Liquidity

- Whether major lenders will finance the property on standard terms

- Any restrictions on loan-to-value ratios

- How the asset is viewed from a resale perspective

4. Local Supply and Competition

- What is currently available in the building

- What is being developed in the surrounding area

- The level of competing stock likely to come to market

Each of these factors contributes to the overall risk profile.

Individually, they may seem manageable.

Combined, they determine the long-term performance of the asset.

A Balanced View

It’s important to be clear.

Apartments are not inherently problematic.

In many cases, they represent a practical, efficient, and well-located form of housing — particularly in a city like Sydney.

Where apartments tend to perform well is in environments where:

- Supply is constrained

- Owner-occupier demand is strong

- Buildings are smaller and better governed

- Financial management is disciplined

- Construction quality is consistent

These are typically boutique or tightly held buildings in established suburbs.

By contrast, higher-density developments in areas with significant future supply tend to behave differently — not necessarily poorly, but with more variability.

The difference is not always obvious at the point of purchase.

Which is why selection matters.

Apartments are not a single asset class.

They are a spectrum.

At one end, you have well-selected properties that perform consistently over time.

At the other, you have assets that are exposed to a range of structural risks — many of which only become visible after settlement.

The challenge for most buyers is that both can look similar on the surface.

In a rising market, that distinction is less important.

In a more selective market, it becomes critical.

The decision is not whether to buy an apartment.

It is whether you fully understand the one you are buying.

And in the current environment, that understanding is what ultimately determines the outcome.