As house prices spiral across the country, would-be homeowners are forced to make a plan. According to CoreLogic data, in February house prices rose at rates beyond anything we’ve seen in 17 years. Only Darwin and Perth have avoided these vast increases in price.

The property price increases have been driven by the economic recovery following lockdown, low interest rates and government stimulus programmes. The prices could rise still further if the government relaxes the responsible lending rules.

Consumers who had thought they had saved enough to get into the real estate market are suddenly out in the cold. As prices soar, they are looking for additional credit or borrowing from their parents.

Lenders who have pre-approved loans have realized that the mortgage amount will not buy the home that they had dreamed of. So, they need more cash and they’re knocking on the doors of the mortgage providers.

Some lenders who had saved their 20% deposit, discover that the amount they have is no longer adequate to the task. Many will borrow more than 80% of the value of the property. This means that they now also have to pay lenders’ mortgage insurance. This insurance is mandatory where the borrower does not have a deposit of at least 20%

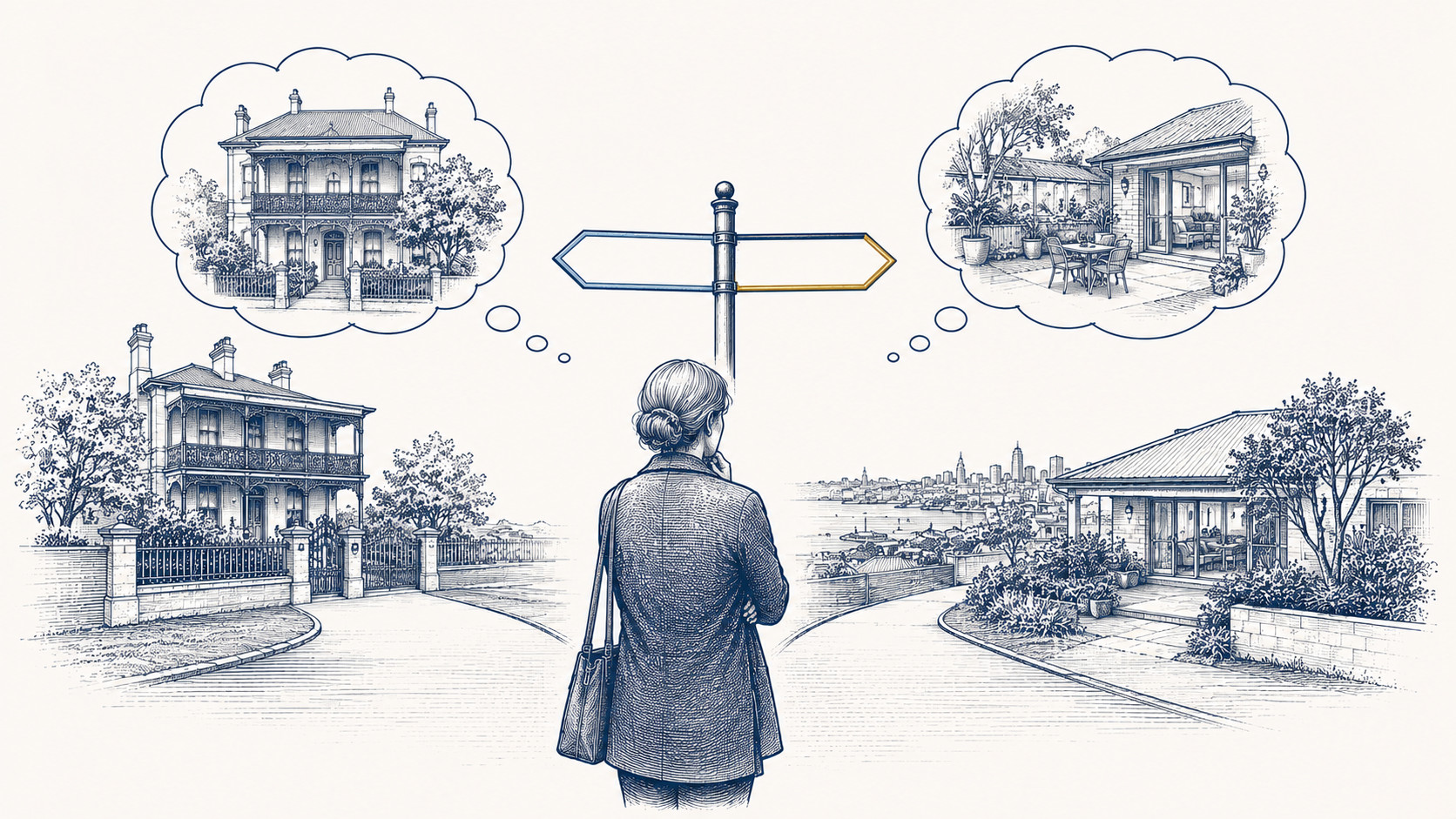

Parents are using their increased home equity to sign guarantor loans for their children. Still, others have gifted the deposit to their offspring to allow them to get a foot into the property markets. An alternative to increased borrowing is to buy down. Buyers may have to do without the spare room or move into a suburb on the outskirts of the city rather than in their preferred location. Otherwise, buyers will have to find someone to lend them the additional funds.